By March 2026, Aave has done something no other DeFi protocol has achieved. It has facilitated over $1 trillion in cumulative loans since its launch. To put that in perspective, that’s more than the GDP of all but 16 countries. And unlike a bank that lends your deposits, every dollar of that trillion was secured by code, not collateralized by trust in a CEO or government bailout.

DeFi lending has entered a new phase. Active loan balances across major protocols now hover near $35‑40 billion – not the brief leverage spikes of previous cycles, but sustained demand across multiple quarters. Aave sits at the center of this structural shift, commanding over 60% of the lending market and processing over $80 million in monthly fees. It has become the system’s core liquidity layer, the place capital flows when the market needs leverage.

In this comprehensive guide Aave explained. We’ll explore how Aave actually works under the hood: the pool‑based lending model, the aTokens that accrue interest in your wallet, the liquidation mechanism that keeps the system solvent, and the groundbreaking V4 upgrade that’s reshaping DeFi’s architecture. By the end, you’ll understand not just what Aave does, but why it has become the most trusted lending protocol in crypto.

Aave in One Sentence

Aave is a decentralized, non‑custodial liquidity protocol where users can earn interest by supplying assets and borrow against their crypto holdings – all governed by smart contracts rather than banks.

Here are a few other ways to think about it:

- For traditional finance people: Aave is like a global, automated money market fund. Depositors earn yield; borrowers post collateral to access liquidity (no credit checks, no branches, just code).

- For crypto people: Aave is the DeFi lending heavyweight – the protocol that pioneered pool‑based lending, flash loans, and now holds over 60% of the market.

- For the curious: Imagine a bank where you can deposit money and earn interest instantly, or borrow against your savings without paperwork, and it runs entirely on software anyone can audit.

The Problem Aave Solves: From Peer-to-Peer to Peer-to-Pool

The Early Days: Peer-to-Peer Lending

Before Aave (and its predecessor ETHLend), decentralized lending was peer‑to‑peer. If you wanted to borrow, you had to find someone willing to lend to you, negotiate terms, and wait for a match. This was slow, illiquid, and inefficient. More like Craigslist than a financial market.

The Innovation: Liquidity Pools

Aave’s breakthrough was the peer‑to‑pool model. Instead of matching individual lenders with individual borrowers, Aave pools all deposited assets into shared liquidity pools. A lender deposits USDC into the pool; a borrower draws from the same pool, posting collateral. The pool always has liquidity. No waiting for a match.

| Traditional Lending | Aave’s Pool Model |

|---|---|

| Matchmaking delays | Instant access |

| Limited liquidity | Deep, aggregated pools |

| Opaque rates | Algorithmically determined |

| Centralized control | Code‑governed, transparent |

The 2026 Context

Today, Aave’s pools hold billions in liquidity. When borrowers demand leverage, capital flows into Aave’s pools. When the market cools, deposits remain sticky. Users have come to trust the protocol as legitimate financial infrastructure, not a speculative vehicle.

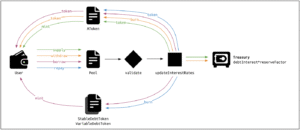

How Aave Works: The Core Mechanism

Supplying Assets and aTokens

When you deposit assets into Aave, you receive aTokens (aUSDC, aETH, etc.) in return. These are interest‑bearing ERC‑20 tokens that automatically increase in value over time as borrowers pay interest.

| Action | Effect |

|---|---|

| You deposit 100 USDC | You receive ~100 aUSDC |

| Borrowers pay interest | aUSDC balance increases (or redemption value rises) |

| You withdraw | Redeem aUSDC for underlying USDC + accrued interest |

Unlike traditional staking where rewards are distributed periodically, aTokens accrue value continuously. If you hold aUSDC for a day, you’ve earned a day’s worth of interest – no claiming, no manual compounding. This makes them ideal for “set and forget” yield strategies.

Your yield comes from borrowers who pay interest, plus a small protocol reserve that funds security and development. The Aave DAO has accumulated significant treasury from these fees, funding initiatives like the $1.5 million V4 audit program.

Borrowing and Over‑Collateralization

Unlike traditional loans that rely on credit scores, Aave loans are always over‑collateralized. To borrow $100 in USDC, you might need to supply $150 in ETH as collateral. This protects the protocol: if your collateral drops in value, the system can sell it to repay your debt.

How borrowing works

- You supply collateral (e.g., ETH) to the protocol.

- You select which asset to borrow (e.g., USDC).

- The protocol checks your Health Factor (collateral value ÷ debt value).

- You receive borrowed assets instantly.

- Your debt is tracked via variableDebtTokens that accrue interest over time.

Why borrowers use Aave

- Leverage: Deposit ETH, borrow USDC, buy more ETH.

- Tax‑efficient liquidity: Borrow against assets without selling (no taxable event).

- Hedging: Borrow stablecoins to short an asset.

- DeFi yield: Borrow to deposit elsewhere for higher yields.

You can repay at any time. Your position remains open as long as your Health Factor stays above 1.0, meaning your collateral value exceeds your debt value by the required margin.

Interest Rates and Utilization

The heartbeat of Aave’s interest rate model is the utilization ratio: total borrows divided by total liquidity in a pool. When utilization is low, rates are low to encourage borrowing. When utilization is high, rates spike to attract more depositors and cool demand.

The two‑slope model

- Below optimal point (e.g., 80%) – rates rise gradually.

- Above optimal point – rates rise steeply.

What this means for users

- Depositors: Higher utilization → higher yields (but also higher risk if borrowers can’t repay).

- Borrowers: Low utilization → cheap borrowing; high utilization → expensive to borrow.

- Protocol: The spread between borrow and deposit rates generates revenue.

Following a peak in late 2024, yields have compressed across DeFi lending. As of early 2026, stablecoin yields on Aave mainnet range from 2.4‑6.5%, with higher yields available on newer chains and through specialized strategies.

Liquidation: The Safety Valve

If your collateral value drops and your debt‑to‑collateral ratio exceeds the protocol’s threshold, your position becomes eligible for liquidation. A liquidator repays part of your debt and receives your collateral at a discount (the liquidation bonus).

Your Health Factor is the critical metric:

Health Factor = (collateral value × liquidation threshold) ÷ debt value

If it falls below 1.0, liquidation is triggered.

Example

- Collateral: 1 ETH ($3,000)

- Liquidation threshold (ETH): 80%

- Borrowed: 2,000 USDC ($2,000)

- Health Factor: (3,000 × 0.8) / 2,000 = 1.2

If ETH drops to $2,500: (2,500 × 0.8) / 2,000 = 1.0 → liquidation threshold hit.

What liquidation means for you

- You lose a portion of collateral (usually 5‑10% bonus to liquidator).

- Your debt is cleared.

- Remaining collateral is returned.

How to avoid liquidation

- Monitor your Health Factor regularly.

- Add more collateral if price drops.

- Repay some debt to lower your position.

- Avoid maxing out borrowing limits.

Aave by the Numbers: 2026 Market Position

| Metric | Value | Significance |

|---|---|---|

| Cumulative loans | $1 trillion | Validates protocol utility over 6+ years |

| Market share | 60%+ | Dominates DeFi lending |

| Active loans | ~$23.2 billion | Real‑time outstanding debt |

| Total deposits (peak) | $125 billion (Oct 2025) | Scale of capital flow |

| Current deposits | ~$79.6 billion | Post‑cooling stabilization |

| Monthly fees | $80 million+ | Sustainable revenue model |

| Daily active users | ~114,600 | Engaged user base |

Active loans across DeFi lending held near cycle highs into early 2026, rising from low single‑digit billions in early 2023 to roughly $35‑40 billion. The key insight: borrowing demand is now sustained across multiple quarters, not driven by short‑term speculation.

The chart of active loans reveals Aave as the system’s core liquidity layer. When leverage demand scales, capital consistently concentrates in Aave’s pools. Its share expands alongside total market growth. This is structural dependence, not episodic usage.

Since October 2025, total deposits have declined approximately $45 billion, with Aave alone accounting for $27.6 billion of that decrease. This reflects a natural market cooldown after Q3 2025 peaks, not protocol stress. Debt remains historically high, and leverage hasn’t unwound aggressively – characteristic of a capital‑driven system.

Key Features That Set Aave Apart

Efficiency Mode (eMode)

Efficiency Mode (eMode) is a V3 feature that dramatically increases capital efficiency when you supply and borrow assets within the same category. For example, stablecoins (USDC/USDT/DAI) or ETH derivatives (ETH/stETH/rETH).

| Feature | Standard Mode | eMode (Correlated Assets) |

|---|---|---|

| Loan‑to‑Value (LTV) | 70‑80% typical | Up to 97% for stablecoins |

| Capital efficiency | Moderate | Maximized |

Example: A user deposits $10,000 in USDC and wants to borrow DAI. In eMode (stablecoin category), they might access up to 97% LTV, borrowing $9,700. Without eMode, they’d be limited to 70‑80% LTV.

Higher leverage means liquidation happens faster if asset prices diverge. For stablecoins, risk is minimal; for ETH derivatives, correlation isn’t perfect, and divergence can trigger liquidation.

Isolation Mode and Siloed Borrowing

When Aave lists a new or volatile asset, it can be placed in Isolation Mode. This asset can only be used as collateral to borrow a specific basket of assets (typically stablecoins), up to a designated debt ceiling. This contains risk while expanding supported assets.

Certain volatile assets can be siloed, borrowers using these assets as collateral can only borrow stablecoins configured for siloed assets, with strict limits. This structure reduces systemic risk by containing exposure.

These risk management features have allowed Aave to expand to over 20 assets across multiple chains without exposing the protocol to cascading failures. It’s one reason Aave has maintained such a dominant market position.

Flash Loans

Flash loans are uncollateralized loans that must be borrowed and repaid within the same transaction. They’re a uniquely DeFi innovation that enables complex financial strategies impossible in traditional finance.

| Feature | Detail |

|---|---|

| Collateral required | None |

| Duration | Single transaction (seconds) |

| Fee | 0.05% of borrowed amount |

| Failure condition | Entire transaction reverts if not repaid |

Use cases

- Arbitrage: Borrow capital, execute profitable trades, repay loan, keep profit.

- Liquidation bots: Repay underwater positions, claim collateral bonuses.

- Collateral swapping: Exchange collateral types without closing positions.

With a 0.05% fee, Aave’s flash loans remain considerably more economical than competing solutions, making them attractive for developers building sophisticated DeFi strategies.

GHO: Aave’s Native Stablecoin

GHO is Aave’s native decentralized stablecoin, minted by users who deposit collateral into the protocol. It’s over‑collateralized, algorithmic, and governed by the Aave DAO.

How it works

- Users deposit collateral (ETH, stETH, etc.) into Aave.

- They mint GHO up to a limit determined by collateral value.

- Interest rates on GHO debt flow to the protocol treasury.

The growth of GHO has played a role in Aave’s expansion. By integrating a debt‑based stablecoin directly into the lending ecosystem, the protocol creates a self‑sustaining cycle: borrowing creates liquidity, which drives total loan metrics.

Aave V4: The Next Evolution

Hub-and-Spoke Architecture

Announced in February 2026, Aave V4 represents the most significant redesign since the protocol’s inception. It introduces a hub‑and‑spoke architecture that fundamentally reimagines DeFi infrastructure.

| Component | Function |

|---|---|

| Central Hub | Manages all liquidity and accounting on each network |

| Spoke Contracts | Plug into the hub, enabling isolated risk for new assets and markets |

This design allows a single hub to serve multiple markets (e.g., Ethereum mainnet, Arbitrum, Base) with spokes that can be deployed independently. The result is unified liquidity. Capital can move seamlessly across markets without fragmentation.

$1.5 Million Security Audit Program

Aave V4 underwent one of the most extensive security reviews in DeFi history.

| Auditor | Scope |

|---|---|

| Sigma Prime | Full‑stack assessment |

| Quantstamp | Smart contract audit |

| ChainSecurity | Economic modeling & governance |

| Trail of Bits | Implementation review |

| Public Contest | Details |

|---|---|

| Duration | 345 days of review |

| Researchers | 900+ participants |

| Submissions | 950+ findings |

| Result | No critical or high‑severity vulnerabilities |

Despite massive review across four major firms and 900+ independent researchers, no critical or high‑severity vulnerabilities were found. This strengthens confidence in the hub‑and‑spoke architecture, which was designed to reduce the protocol’s overall attack surface.

Long‑term security commitments adopted by Aave Labs

- Formal verification from the start of development cycles.

- Layered security methodologies combining multiple auditing techniques.

- Continuous verification alongside development.

- Permanent bug bounty program.

- AI‑assisted smart contract scanning.

Token‑Centric Economics

V4 introduces a token‑centric model designed to increase value capture for AAVE holders. As protocol activity grows, a larger portion of generated revenue flows back to the token and the DAO.

| Before V4 | With V4 |

|---|---|

| Revenue flows primarily to treasury | Enhanced direct value capture for AAVE |

| Token utility largely governance | Stronger economic link to protocol success |

| Less alignment | Better incentives for long‑term holders |

By strengthening the token’s economic fundamentals, the new model aims to enhance Aave DAO’s resilience and effectiveness, providing stronger incentives for participation and security.

Horizon: Aave’s Institutional On‑Ramp

Horizon is Aave’s permissioned market designed specifically for institutional participants. It allows regulated entities to access Aave’s liquidity infrastructure while maintaining compliance requirements.

| Metric | Status |

|---|---|

| Current net deposits | $550 million |

| 2026 target | $1 billion |

| Key partners | BlackRock, Franklin Templeton |

How Horizon works

- Institutions supply tokenized real‑world assets (RWAs) as collateral.

- They access permissionless stablecoin liquidity.

- Identity verification and compliance checks are required.

- Risk monitoring uses institutional‑grade tools with real‑time NAV validation.

Projections suggest $100 billion in RWA tokenization by 2030. Horizon positions Aave to capture institutional demand for onchain credit markets, bringing traditional capital into DeFi.

BlackRock’s BUILD fund and Franklin Templeton’s FOBXX are among the RWAs being integrated. This marks a significant shift from DeFi as a retail phenomenon to core financial infrastructure.

The Risks of Using Aave (Important!)

⚠️ CRITICAL SECTION. DO NOT SKIP

Risk 1: Liquidation Risk (Most Common)

Your position can be liquidated if your Health Factor drops below 1.0. During volatile markets, this can happen suddenly, and you lose a portion of your collateral.

Mitigation: Monitor Health Factor regularly. Never borrow to your maximum limit. Add collateral during drawdowns.

Risk 2: Smart Contract Vulnerability

Despite extensive audits, no code is completely risk‑free. A critical vulnerability could lead to loss of funds. Aave’s $1.5 million audit program and 345 days of review significantly reduce this risk, but it cannot be eliminated.

Risk 3: Oracle Failure

Aave relies on price oracles to value collateral and trigger liquidations. If oracles fail or are manipulated, positions could be liquidated incorrectly or under‑collateralized loans could go undetected.

Risk 4: Interest Rate Volatility

Borrow rates can spike dramatically during periods of high utilization. Your debt can become more expensive faster than expected.

Risk 5: Protocol Governance Risk

AAVE token holders govern protocol parameters. Poor governance decisions could affect your positions. Recent tensions within the Aave DAO over funding and direction highlight this as an active concern.

Risk 6: Regulatory Uncertainty

While the SEC closed its four‑year investigation into Aave without enforcement action, regulatory frameworks continue to evolve globally. Future restrictions could affect access.

Risk 7: Smart Contract Slippage

Flash loan attacks and sophisticated exploits have targeted DeFi protocols historically. Aave’s security track record is strong, but the threat remains.

The Safety Checklist

- Start small – test with amounts you can afford to lose.

- Monitor your Health Factor (use DeFi portfolio trackers).

- Never borrow to your maximum limit.

- Understand the assets you’re supplying and borrowing.

- Use only trusted front‑ends (

app.aave.com). - Keep a buffer in case of rapid market moves.

How to Use Aave: Step‑by‑Step Guide

Step 1: Set Up a Wallet

You’ll need a non‑custodial wallet like MetaMask, Rabby, or Coinbase Wallet. Fund it with Ethereum or another chain’s native token for gas fees.

Step 2: Choose Your Network

Aave operates across multiple chains: Ethereum mainnet, Arbitrum, Base, Polygon, Avalanche, and others. Ethereum mainnet has the deepest liquidity; Layer 2s offer lower fees.

Step 3: Supply Assets to Earn Yield

- Go to app.aave.com (bookmark the official URL).

- Connect your wallet.

- Select the asset you want to supply.

- Click “Supply” and enter amount.

- Confirm the transaction.

- You’ll receive aTokens in your wallet that accrue interest.

Step 4: Borrow Against Your Collateral

- After supplying, navigate to the “Borrow” tab.

- Select the asset you want to borrow.

- Review your Health Factor and available borrow limit.

- Enter amount and confirm.

- Your debt begins accruing interest immediately.

Step 5: Monitor Your Position

- Track your Health Factor in the dashboard.

- Set alerts for significant price moves (use DeFi portfolio trackers).

- Add collateral or repay debt if Health Factor approaches 1.0.

Step 6: Withdraw or Repay

- To withdraw supplied assets: Navigate to “Dashboard,” select your position, and click “Withdraw.”

- To repay borrowed assets: Navigate to “Dashboard,” select your debt, and click “Repay.”

Pro Tips for Beginners

| Tip | Why It Matters |

|---|---|

| Start on Layer 2 | Lower gas fees on Arbitrum, Base, or Polygon |

| Use stablecoins first | Less volatility, easier to learn mechanics |

| Never max out borrow | Keep Health Factor above 1.5 |

| Test with small amounts | Learn before committing significant capital |

Recommended Resources

- Official Aave docs: docs.aave.com

- DeFi portfolio trackers: DeBank, Zapper

The Future of Aave

2026 Roadmap

| Initiative | Timeline | Impact |

|---|---|---|

| V4 Launch | 2026 | Hub‑and‑spoke architecture, unified liquidity |

| Horizon expansion | 2026 | $1B institutional RWA deposits |

| Aave App launch | 2026 | Mobile‑first onboarding for 1M users |

| Multi‑chain expansion | Ongoing | Deeper L2 integration |

From Speculation to Infrastructure

Aave has evolved from a yield farming destination to core financial infrastructure. Active loans remaining elevated across quarters -despite market cooldowns – signals durable borrow demand and structural dependence on the protocol.

The Institutional Pivot

With Horizon targeting institutional RWAs and the SEC investigation closed without action, Aave is positioned at the intersection of traditional and decentralized finance. The question isn’t whether institutions will use DeFi, it’s whether Aave will be their on‑ramp.

Founder’s Vision

Aave founder Stani Kulechov recently purchased between $9.8 million and $15 million in AAVE tokens, signaling confidence in the protocol’s future despite governance tensions. His vision: Aave as the default ledger for both retail and institutional finance.

Next Steps: From Learning to Participating

You now understand Aave. Here’s where to go next:

| Step | Action | Resource |

|---|---|---|

| 1. Get a Wallet | MetaMask or Rabby | Wallet Guide |

| 2. Acquire Assets | ETH, USDC, or other supported tokens | How to Buy Crypto |

| 3. Start on L2 | Bridge to Arbitrum or Base for lower fees | Layer 2 Guide |

| 4. Supply Small Amount | Test with $50‑100 to understand mechanics | Aave app |

| 5. Monitor Position | Use DeBank or Zapper for tracking | Portfolio tools |

Essential Next Reads

- 📚 What is DeFi? A Beginner’s Guide

- 📚 Liquid Staking Explained: Lido and Rocket Pool

- 📚 How to Avoid Crypto Scams: Complete Guide

- 📚 Layer 2 Scaling: Ethereum’s Future

Join the Community

Aave’s governance and development happen in public. Join the Aave Discord, follow the governance forum, and subscribe to our newsletter for weekly DeFi updates.

Final Thought

Aave isn’t just a lending protocol, it’s the liquidity layer that underpins much of DeFi. Whether you’re earning yield on stablecoins, borrowing against ETH without selling, or watching institutional capital flow into RWAs, Aave is where the action is.

Start small, stay informed, and let your crypto work for you.

Disclaimer: This guide is for educational purposes only and does not constitute financial advice. Decentralized finance involves significant risks, including potential loss of funds. Always do your own research and never invest more than you can afford to lose.

This guide was last updated for the 2026 edition. Aave evolves rapidly – new features, markets, and governance decisions happen regularly. Always verify current information on the official Aave website and documentation.

Frequently Asked Questions

Is Aave safe to use?

Aave is one of the most battle‑tested protocols in DeFi with over $1 trillion in cumulative loans and no major hacks. The V4 audit program cost $1.5 million and found no critical vulnerabilities. However, risks remain: liquidation, smart contract bugs, and oracle failures are all possible. Never invest more than you can afford to lose.

What is the difference between supplying and borrowing?

Supplying means depositing assets into Aave’s liquidity pools to earn yield. Borrowing means taking a loan against your supplied assets (collateral). Borrowing requires over‑collateralization. You must supply more value than you borrow.

How do aTokens work?

aTokens are interest‑bearing tokens you receive when you supply assets. They automatically increase in value over time as borrowers pay interest. When you withdraw, you redeem aTokens for the underlying asset plus accrued yield.

What is the utilization rate in Aave?

Utilization = total borrows divided by total liquidity in a pool. It determines interest rates: low utilization = low rates; high utilization = higher rates to attract more deposits.

How does Aave liquidation work?

If your Health Factor falls below 1.0 (collateral value too low relative to debt), liquidators can repay your debt and receive your collateral at a discount (liquidation bonus). You lose part of your collateral, and your debt is cleared.

What is efficiency mode (eMode) in Aave?

eMode allows higher borrowing capacity when you supply and borrow correlated assets (like stablecoins or ETH derivatives). You can achieve up to 97% LTV on stablecoin pairs, maximizing capital efficiency.

How much can I earn supplying USDC on Aave?

As of March 2026, stablecoin yields on Aave mainnet range from 2.4‑6.5% APY, depending on utilization and market conditions. Higher yields are available on newer chains or through specialized strategies.

What is the Aave GHO stablecoin?

GHO is Aave’s native decentralized stablecoin, minted by users who deposit collateral. It’s over‑collateralized, governed by the Aave DAO, and integrates directly with the lending ecosystem.

What is Aave V4?

Aave V4 is the next major protocol upgrade, announced in February 2026. It introduces a hub‑and‑spoke architecture for unified liquidity, a token‑centric economic model, and underwent a $1.5 million security audit with no critical findings.

What is the Horizon platform?

Horizon is Aave’s permissioned market for institutional real‑world assets. It allows regulated entities to use tokenized bonds and funds as collateral to borrow stablecoins, with $550 million in deposits and a $1 billion 2026 target.

Did the SEC investigate Aave?

Yes, the SEC closed a four‑year investigation into Aave in late 2025 without enforcement action. This outcome is viewed as a major validation of decentralized protocol structures.

How do I avoid liquidation on Aave?

Monitor your Health Factor, add more collateral if prices drop, repay some debt to reduce your position, and never borrow to your maximum limit. Keep a buffer of at least 30%.

What chains is Aave available on?

Aave operates on Ethereum mainnet, Arbitrum, Base, Polygon, Avalanche, and several other networks. V3 supports 14+ chains, with V4 expanding further.

Is Aave better than Compound?

Aave holds over 60% market share, surpassing Compound and all competitors combined. Aave offers more features (eMode, flash loans, GHO) and has shown stronger resilience and growth.

1 thought on “Aave Explained: Lending and Borrowing in DeFi (2026 Complete Guide)”