Imagine being able to lend your savings and earn 5% interest without a bank taking a cut. Imagine borrowing money by putting up collateral, with no credit check and instant approval. Imagine trading assets directly with another person, no middleman, no waiting days for settlement.

This isn’t a futuristic fantasy, it’s DeFi, and it’s happening right now on public blockchains.

I remember my first DeFi transaction. I’d been in crypto for years, but always just buying and holding. Then I deposited some ETH into Aave, watched the interest accumulate in real-time, and realized: this is different. I wasn’t just speculating on price. I was actually using financial infrastructure – earning yield, providing liquidity, participating in a system that ran entirely on code.

DeFi, short for Decentralized Finance, refers to financial applications built on blockchain technology that operate without traditional intermediaries like banks, brokers, or exchanges. Instead, they use smart contracts, self-executing code, to automate financial services that anyone with an internet connection can access.

In this guide, we’ll explain what is DeFi in plain English: how it works, what you can do with it (lend, borrow, trade, earn), the risks you need to understand, and how to get started safely.

DeFi in One Sentence

DeFi (Decentralized Finance) is a system of financial applications built on blockchain networks, primarily Ethereum, that lets you lend, borrow, trade, and earn interest on cryptocurrency without relying on banks, brokers, or any centralized authority.

Here are a few other ways to think about it:

- For traditional finance people: DeFi is like having a bank that runs entirely on code – no tellers, no loan officers, no branches, just automated financial services available 24/7 to anyone with an internet connection.

- For crypto people: DeFi takes the principles of Bitcoin – decentralization, transparency, self-custody and applies them to the entire financial system: lending, borrowing, trading, and more.

- For the curious: Imagine if your savings account, your stock broker, and your currency exchange were all combined into one app that you control completely, with no company in the middle taking a cut.

The Problem DeFi Solves

The Traditional Finance Problem

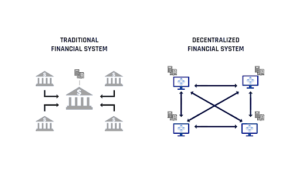

Traditional finance relies on intermediaries, banks, brokers, clearinghouses, to facilitate transactions. These intermediaries serve important functions (verification, record-keeping, risk management), but they come with significant drawbacks:

| Problem | Example |

|---|---|

| Limited access | 1.4 billion adults worldwide are unbanked |

| Slow settlement | International wire transfers take days |

| High fees | Banks charge for accounts, loans, transfers |

| Opaque operations | You don’t know how banks use your money |

| Censorship | Banks can freeze accounts, block transactions |

| Limited hours | Markets close on weekends, holidays |

How DeFi Solves These Problems

| DeFi Solution | How It Works |

|---|---|

| Permissionless access | Anyone with an internet connection and a wallet can participate (no ID required) |

| Instant settlement | Transactions settle in seconds or minutes, 24/7/365 |

| Lower fees | No overhead of physical branches, fewer intermediaries |

| Full transparency | All transactions are public on the blockchain; smart contract code is visible |

| Censorship resistance | No single entity can block your transactions |

| Always open | DeFi never sleeps. Trade, lend, borrow anytime |

The Core Innovation

DeFi doesn’t just digitize finance, it democratizes it. For the first time in history, anyone with an internet connection can access sophisticated financial services previously available only to accredited investors or residents of wealthy countries.

How DeFi Works: Smart Contracts Are the Key

The Building Blocks

DeFi applications (called “protocols” or “dApps”) are built on smart contract platforms, primarily Ethereum, but also Solana, Avalanche, and others. Smart contracts are self-executing code that automatically enforce the terms of an agreement.

The Vending Machine Analogy

A smart contract is like a vending machine:

- You put money in (deposit crypto)

- You select a product (choose a financial service)

- The machine automatically gives you what you selected

- No human interaction required

- The machine follows its programming exactly. No negotiation, no exceptions

How a Typical DeFi Transaction Works

- You connect your wallet (MetaMask, Trust Wallet, etc.) to a DeFi application

- You approve a transaction (e.g., depositing ETH into a lending protocol)

- The smart contract executes – your ETH is locked in the protocol, and you receive a token representing your deposit

- You earn yield as the protocol lends your assets to borrowers

- You withdraw by returning the token; the smart contract releases your ETH plus earned interest

Key Components of DeFi

| Component | Function |

|---|---|

| Smart Contracts | The code that runs DeFi applications – transparent, immutable, autonomous |

| Wallets | Your interface to DeFi; holds your private keys and connects to dApps |

| Oracles | Services that bring real-world data (prices) onto the blockchain |

| Governance Tokens | Tokens that let users vote on protocol changes |

| Liquidity Pools | Pools of funds supplied by users that enable trading and lending |

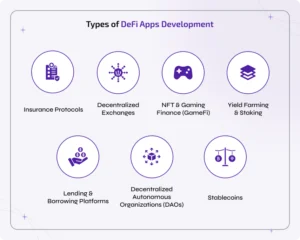

Key DeFi Applications

Decentralized Exchanges (DEXs)

What They Are: DEXs like Uniswap, Curve, and PancakeSwap let you trade cryptocurrencies directly from your wallet. No account, no KYC, no withdrawal limits. You retain custody of your funds at all times.

How They Work: Instead of using an order book (like Coinbase or Binance), most DEXs use Automated Market Makers (AMMs) –smart contracts that hold pools of tokens and set prices algorithmically based on supply and demand.

Why They Matter:

- No exchange holds your funds (reduces exchange hack risk)

- Anyone can list any token (but also means scam tokens exist)

- Available 24/7 globally

Example: You want to swap ETH for USDC. You connect to Uniswap, select the pair, and confirm the transaction. The swap executes instantly, and your USDC appears in your wallet.

Lending and Borrowing Platforms

What They Are: Protocols like Aave and Compound let you lend your crypto to earn interest or borrow against your holdings without selling.

How Lending Works: You deposit your crypto into a lending pool. The protocol automatically lends it to borrowers. You receive a token (like aUSDC or cETH) representing your deposit, which accrues interest in real-time.

How Borrowing Works: You deposit collateral (e.g., ETH) and borrow a different asset (e.g., USDC). Your loan is over-collateralized, typically 150%, meaning you must deposit $150 of ETH to borrow $100 of USDC. This protects lenders from default.

Why It Matters:

- Earn passive income on idle assets

- Access liquidity without selling your crypto (tax-efficient)

- No credit checks, no paperwork

⚠️ WARNING: Borrowing carries liquidation risk. If your collateral value drops below the required threshold, the protocol automatically sells it to repay your loan.

Staking and Yield Farming

Staking (Simple): Staking means locking your crypto in a proof-of-stake network (like Ethereum, Solana, or Cardano) to help secure it and earn rewards. Many DeFi protocols also offer “liquid staking”. You stake through a service like Lido or Rocket Pool and receive a tradable token representing your staked position.

Yield Farming (More Advanced): Yield farming involves moving your crypto between different DeFi protocols to maximize returns. Farmers chase the highest yields, often earning protocol governance tokens in addition to interest.

Example: A yield farmer might deposit USDC into Aave, receive aUSDC, then deposit that aUSDC into another protocol for additional rewards. Returns can be high, but risks multiply.

Risks:

- Smart contract risk (bugs in any protocol in the chain)

- Impermanent loss (when providing liquidity)

- Gas fees can eat profits (especially on Ethereum)

Stablecoins

What They Are: Stablecoins are cryptocurrencies designed to maintain a stable value (usually pegged 1:1 to the US dollar). They’re the backbone of DeFi, providing a stable medium of exchange and store of value.

Types of Stablecoins:

| Type | Example | How It Works |

|---|---|---|

| Fiat-backed | USDT, USDC | Backed by actual dollars or equivalents in bank accounts |

| Crypto-backed | DAI | Over-collateralized with crypto; decentralized |

| Algorithmic | (Most failed after UST collapse) | Use algorithms to maintain peg (highly risky) |

Why They Matter in DeFi:

- Provide stability in a volatile ecosystem

- Enable lending/borrowing with predictable units

- Used for trading pairs, payments, and yield generation

⚠️ WARNING: Not all stablecoins are equally safe. USDC and USDT are considered safer but are centralized. DAI is decentralized but backed by volatile crypto. Algorithmic stablecoins have a history of catastrophic failures.

Derivatives and Synthetic Assets

What They Are: Derivatives platforms like dYdX, Synthetix, and GMX let you trade futures, options, and synthetic versions of real-world assets (stocks, commodities, currencies) on-chain.

Examples:

- Trade Bitcoin perpetual futures with leverage

- Get exposure to Tesla stock without buying actual shares (via synthetic assets)

- Short Ethereum without borrowing the asset

Why It Matters:

- Access to advanced trading strategies

- Exposure to traditional assets without leaving crypto

- 24/7 markets, no broker

⚠️ WARNING: Derivatives are complex and high-risk. Leverage amplifies both gains and losses. Not for beginners.

DeFi vs Traditional Finance: A Comparison

| Feature | Traditional Finance | DeFi |

|---|---|---|

| Access | Requires ID, credit check, bank account | Anyone with internet and a wallet |

| Custody | Bank holds your money | You hold your private keys |

| Hours | 9-5, weekdays, holidays closed | 24/7/365, never closes |

| Settlement | Days (international) | Seconds to minutes |

| Transparency | Opaque – you don’t know how bank operates | Fully transparent – code and transactions public |

| Fees | Often high, opaque | Generally lower, transparent |

| Censorship | Banks can freeze accounts | Transactions can’t be blocked |

| Interest rates | Set by banks, typically low | Market-driven, often higher |

| Risk | Bank failure (insured up to $250k) | Smart contract bugs, hacks, volatility |

The Trade-offs

| DeFi Advantage | DeFi Disadvantage |

|---|---|

| Higher potential returns | Higher risk (smart contract bugs) |

| Full control of assets | Full responsibility (lose keys = lose funds) |

| Access to innovative products | Complex, steep learning curve |

| Global, permissionless | Regulatory uncertainty |

| Transparent | Some protocols have hidden risks |

The Bottom Line

DeFi isn’t trying to replace traditional finance overnight. It’s offering an alternative system with different trade-offs. For those who value control, transparency, and access, DeFi is revolutionary. For those who prefer the safety and simplicity of banks, traditional finance may still be the better fit.

What is Total Value Locked (TVL)?

Definition

Total Value Locked (TVL) is the most important metric in DeFi. It measures the total value of assets deposited in a DeFi protocol, usually expressed in USD. Think of it as the “assets under management” for decentralized finance.

Why TVL Matters

| TVL Signal | What It Indicates |

|---|---|

| High and growing TVL | User trust, protocol adoption, liquidity |

| Declining TVL | Users withdrawing funds – could signal problems |

| TVL by chain | Which blockchains host the most DeFi activity |

Current TVL (March 2026)

Total DeFi TVL across all chains is approximately $99 billion, down from peaks over $100 billion but still representing a mature, resilient ecosystem. Ethereum dominates with ~55% of TVL, followed by Solana, Arbitrum, and BNB Chain.

Top Protocols by TVL

| Protocol | Type | Approximate TVL |

|---|---|---|

| Lido | Liquid Staking | $20B+ |

| Aave | Lending | $10B+ |

| EigenLayer | Restaking | $7B+ |

| MakerDAO | Stablecoin (DAI) | $5B+ |

| Uniswap | DEX | $4B+ |

Where to Check TVL

Real-time TVL data is available on aggregators like DefiLlama and DappRadar. These sites also show TVL trends, chain breakdowns, and protocol comparisons.

Real-World Assets (RWAs): The 2026 Evolution

The Next Frontier

One of the most significant DeFi trends in 2026 is the integration of Real-World Assets (RWAs) – tokenized versions of traditional financial instruments like Treasury bonds, real estate, commodities, and private credit.

Why RWAs Matter

| Traditional Asset | DeFi RWA Equivalent |

|---|---|

| US Treasury bonds | Tokenized Treasuries (via Ondo, Maple) |

| Corporate bonds | Tokenized credit |

| Real estate | Property-backed tokens |

| Commodities | Gold, oil tokens |

The Institutional On-Ramp

RWAs bridge the gap between traditional finance and DeFi. Institutional investors can earn yield on-chain without leaving their comfort zone of regulated assets. DeFi protocols gain access to stable, real-world collateral, reducing volatility.

Key RWA Protocols (2026)

| Protocol | Focus | TVL/Volume |

|---|---|---|

| Ondo Finance | Tokenized Treasuries | $2.7B+ |

| Maple Finance | Institutional lending | $2.39B+ |

| Centrifuge | Real-world asset lending | $1.24B+ |

| MakerDAO | RWA collateral (T-bills) | $7.5B+ |

The Significance

Analysts project that RWAs could bring trillions of dollars in traditional assets onto blockchains over the next decade. For DeFi, this means:

- More stable collateral

- Institutional participation

- Yield opportunities uncorrelated with crypto volatility

The Risks of DeFi (Important!)

⚠️ CRITICAL SECTION. DO NOT SKIP

Risk 1: Smart Contract Vulnerabilities

DeFi protocols are code, and code can have bugs. A single vulnerability can lead to millions in lost funds. Major hacks have drained billions from DeFi over the years.

Examples:

- 2022 Ronin Bridge hack: $625M

- 2023 Euler Finance exploit: $197M

- 2024 Various bridge and lending protocol hacks

Mitigation:

- Use well-audited protocols with proven track records

- Look for protocols with bug bounties, insurance funds

- Smaller, newer protocols carry higher risk

Risk 2: Impermanent Loss

When you provide liquidity to a DEX, you risk impermanent loss. The temporary loss of value compared to simply holding your assets. This occurs when the price ratio of your deposited assets changes.

Simple Explanation: If you deposit ETH and USDC into a pool, and ETH doubles in price, you’d have been better off just holding ETH. The protocol’s algorithm ensures the pool maintains balance, so you end up with less ETH and more USDC than you started with.

Risk 3: Liquidation Risk (for Borrowers)

If you borrow against your crypto and the price drops sharply, your position can be liquidated. The protocol automatically sells your collateral to repay the loan. You lose your collateral and still owe nothing (the loan is cleared).

Risk 4: Regulatory Risk

DeFi operates in a gray area globally. Future regulations could restrict access, tax certain activities, or deem some protocols illegal. The US, EU, and Asia are all developing crypto regulatory frameworks.

Risk 5: Scams and Rug Pulls

Because anyone can create a DeFi protocol, scams are common. “Rug pulls” occur when developers drain liquidity pools and disappear with users’ funds.

Red Flags:

- Anonymous teams (no public identities)

- Unaudited code

- Promises of unrealistic returns

- No clear business model

Risk 6: User Error

In DeFi, you are your own bank. Lose your private keys, send funds to the wrong address, or interact with a malicious contract, your funds are gone forever. There’s no customer support to call.

Risk 7: Gas Fees

On Ethereum, transaction fees (gas) can spike during congestion, making small transactions uneconomical. Layer 2 solutions (Arbitrum, Optimism, Base) reduce fees but add complexity.

The Golden Rule

Never invest more than you can afford to lose. Start with small amounts to learn. Understand each protocol before depositing funds. DeFi offers opportunity, but it demands responsibility.

How to Get Started with DeFi

The Beginner’s Path

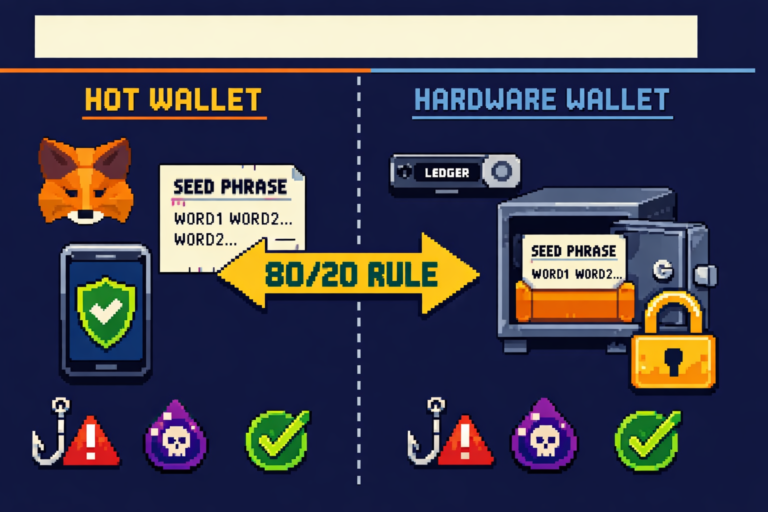

Step 1: Get a Wallet

You need a non-custodial wallet to interact with DeFi. MetaMask (Ethereum and EVM chains) and Phantom (Solana) are the most popular choices.

- Download from official sources only

- Write down your seed phrase on paper. Never digitally

- Start with small amounts

📚 What is a Crypto Wallet? Hot vs Cold Storage Explained

Step 2: Fund Your Wallet

You’ll need cryptocurrency to participate. Buy ETH, SOL, or other native tokens on a centralized exchange (Coinbase, Kraken) and transfer to your wallet.

📚 How to Buy Cryptocurrency: Step-by-Step Guide

Step 3: Choose a Chain

Most DeFi activity happens on Ethereum and its Layer 2s (Arbitrum, Optimism, Base). Solana offers a faster, cheaper alternative. Each chain has different protocols, fees, and learning curves.

Step 4: Start Simple

| Beginner Activity | Protocol Example | What You’ll Learn |

|---|---|---|

| Swap tokens | Uniswap | DEX basics, gas fees |

| Provide liquidity | Uniswap (one pool) | Impermanent loss |

| Lend stablecoins | Aave | Passive yield, borrowing |

| Stake ETH | Lido | Liquid staking |

Step 5: Start Small

Deposit $50-100 to test the waters. Learn how approvals work, how to track your positions, and how to withdraw. Once comfortable, you can increase exposure.

Step 6: Explore Layer 2s

Ethereum gas fees can be high. Bridge your assets to Arbitrum, Optimism, or Base for cheaper transactions. Many protocols now operate across multiple L2s.

Step 7: Track Your Portfolio

Use tools like DeBank, Zapper, or Zerion to track your DeFi positions across multiple protocols and chains in one dashboard.

Essential Tools

| Tool | Purpose |

|---|---|

| DeBank | Portfolio tracker, protocol analytics |

| DefiLlama | TVL data, protocol comparisons |

| RugDoc | Security reviews, risk assessments |

| Etherscan | Transaction verification |

DeFi Terminology Cheat Sheet

| Term | Definition |

|---|---|

| APR/APY | Annual Percentage Rate/Yield – measures expected returns |

| AMM | Automated Market Maker – DEX that uses liquidity pools instead of order books |

| Collateral | Assets you deposit to secure a loan |

| DEX | Decentralized Exchange (Uniswap, PancakeSwap) |

| Gas | Transaction fees paid to blockchain validators |

| IL | Impermanent Loss – temporary loss from liquidity provision |

| L1/L2 | Layer 1 (base blockchain) / Layer 2 (scaling solution) |

| Liquidity Pool | Pool of tokens locked in a smart contract enabling trading |

| LP Token | Token representing your share of a liquidity pool |

| Oracles | Services that feed real-world data (prices) to blockchains |

| Rug Pull | Scam where developers steal user funds |

| RWA | Real-World Assets – tokenized traditional assets |

| Staking | Locking tokens to support a network/protocol and earn rewards |

| TVL | Total Value Locked – assets deposited in a protocol |

| Wallet | Interface for interacting with blockchain, holds private keys |

| Yield Farming | Moving funds between protocols to maximize returns |

Next Steps: From Learning to Participating

You now understand DeFi. Here’s where to go next:

The Beginner’s Path

| Step | Action | Resource |

|---|---|---|

| 1. Get a Wallet | Download MetaMask or Phantom | Wallet Guide |

| 2. Fund It | Buy ETH/SOL on exchange, transfer | Exchange Guide |

| 3. Start Simple | Try swapping on Uniswap | Uniswap Guide |

| 4. Earn Yield | Lend stablecoins on Aave | Aave Guide |

| 5. Explore L2s | Bridge to Arbitrum for lower fees | L2 Guide |

| 6. Track Positions | Use DeBank or Zapper | DeFi Tools Guide |

Essential Next Reads

- 📚 What is Uniswap? A Beginner’s Guide to DEXs

- 📚 Aave Explained: Lending and Borrowing in DeFi

- 📚 Staking vs Yield Farming: What’s the Difference?

- 📚 Layer 2 Scaling: Ethereum’s Future

Join the Community

DeFi moves fast. Join our Discord, follow us on Twitter, and subscribe to our newsletter for weekly DeFi updates, new protocol launches, and security alerts.

Final Thought

When I made my first DeFi deposit, I was nervous. I double-checked every address, every approval, every transaction. But when I saw that interest start accruing – automatically, transparently, without any bank telling me what rate I’d get, I understood.

DeFi is the most exciting innovation in finance since the internet itself. It’s not without risks, but for those willing to learn, it offers unprecedented access, control, and opportunity.

Start small, stay curious, and welcome to the future of finance.

Disclaimer: This guide is for educational purposes only and does not constitute financial advice. DeFi involves significant risks, including potential loss of funds. Always do your own research and never invest more than you can afford to lose.

This guide was last updated for the 2026 edition. DeFi evolves rapidly – protocols come and go, yields change, and new risks emerge. Always verify information with multiple sources before depositing funds.

Frequently Asked Questions

How does DeFi make money?

DeFi protocols generate revenue through fees: trading fees on DEXs, interest rate spreads on lending platforms, and protocol fees on various services. Users who supply liquidity or stake governance tokens earn a share of these fees.

Is DeFi safe for beginners?

DeFi carries significant risks, including smart contract bugs, hacks, impermanent loss, and user error. Beginners should start with small amounts on established protocols (Uniswap, Aave), use hardware wallets for security, and never invest more than they can afford to lose.

What can you do with DeFi?

DeFi enables a wide range of financial activities: trading (DEXs), lending and borrowing, earning yield (staking, farming), using stablecoins, trading derivatives, and accessing synthetic versions of traditional assets.

How do I start using DeFi?

Get a non-custodial wallet (MetaMask), fund it with crypto from an exchange, choose a blockchain (Ethereum or Solana), and start with simple activities like swapping tokens on Uniswap or lending on Aave. Always start small.

What is a decentralized exchange (DEX)?

A DEX is a cryptocurrency exchange that operates without a central authority. You trade directly from your wallet using smart contracts. Examples: Uniswap, PancakeSwap, Curve.

What is yield farming in crypto?

Yield farming is the practice of moving your crypto between different DeFi protocols to maximize returns. Farmers earn interest, trading fees, and governance tokens. It's more complex and risky than simple staking.

What are the risks of DeFi?

Major risks include: smart contract bugs/hacks, impermanent loss, liquidation (for borrowers), regulatory uncertainty, scams/rug pulls, user error, and high gas fees during congestion.

How is DeFi different from a bank?

Banks are centralized intermediaries. They hold your money, set rates, and operate during business hours. DeFi is code-based: you control your funds, rates are market-driven, and services run 24/7. Banks offer FDIC insurance; DeFi offers no such protection.

What is total value locked (TVL)?

TVL measures the total value of assets deposited in DeFi protocols. It's like "assets under management" for decentralized finance. Higher TVL generally indicates more user trust and liquidity.

Is DeFi legal?

DeFi operates in a regulatory gray area globally. Using DeFi protocols is generally legal for individuals, but regulations vary by country. Some protocols restrict access from certain jurisdictions (like the US) due to regulatory uncertainty.

What are the best DeFi protocols for beginners?

Start with established protocols: Uniswap (DEX), Aave (lending), Lido (staking), and Curve (stablecoin DEX). These have long track records, high TVL, and extensive documentation.

Do I need a lot of money to use DeFi?

No. You can start with as little as $50-100, though Ethereum gas fees may make small transactions uneconomical. Consider using Layer 2 solutions (Arbitrum, Optimism) or Solana for lower fees.

Can I lose money in DeFi?

Yes. Beyond market volatility, you can lose funds to smart contract hacks, impermanent loss, liquidation, scams, or user error. Never invest more than you can afford to lose.

What is the future of DeFi?

The future includes deeper integration with traditional finance through Real-World Assets (RWAs) , more institutional participation, improved security through audits and insurance, better user experience, and continued regulatory evolution.

2 thoughts on “What is DeFi? Decentralized Finance Explained (2026 Beginner’s Guide)”