Imagine you’re keeping track of IOUs with friends. You write everything in a notebook. Every time someone pays someone back, you update the notebook.

But what if you lose it? What if someone changes the numbers when you’re not looking? What if your friend claims they paid you back, but you forgot to record it?

Now imagine that instead of one notebook, everyone has an identical copy. Every time someone pays someone else, everyone writes it down together at the same time. To change a record, you’d need to change every single notebook at exactly the same moment. Impossible without everyone noticing.

That’s blockchain.

When I first heard the word “blockchain,” I assumed it was incomprehensible, something only programmers with math PhDs could understand. Then someone explained it using the Google Docs analogy (which you’ll see in a moment), and suddenly it clicked. Blockchain isn’t complicated because the idea is hard. It’s complicated because we’ve never had a system quite like it before.

In this guide, we’ll explain what is blockchain technology in plain English, how it works, why it’s secure, and why it matters far beyond cryptocurrency. No coding knowledge required. Just curiosity.

Blockchain in One Sentence

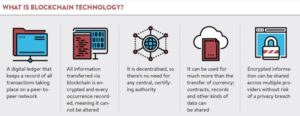

A blockchain is a shared digital record book that multiple computers maintain together, where entries are permanent, transparent, and impossible to change once recorded.

Here are a few other ways to think about it:

- For business people: A blockchain is a decentralized database that multiple parties trust because no single party controls it.

- For tech people: A blockchain is a distributed, immutable ledger that records transactions across a peer-to-peer network using cryptographic verification.

- For the curious: Imagine a notebook that everyone in the world can see, anyone can add to, but no one can erase.That’s blockchain.

The Problem Blockchain Solves

The Trust Problem

For thousands of years, whenever two people wanted to exchange value or make an agreement, they needed a trusted third party:

- Banks verify transactions between people

- Governments record property ownership

- Lawyers draft and verify contracts

- Notaries certify documents

- Escrow agents hold funds until conditions are met

These intermediaries work, but they have problems:

- They charge fees (sometimes substantial)

- They can make mistakes

- They can be corrupted or compromised

- They can be hacked

- They can censor or block transactions

The Centralization Problem

Today, most of our data is centralized. One company controls it:

- Facebook controls your social data

- Your bank controls your money

- Amazon controls your purchase history

- Google controls your emails

If that company is breached, your data is exposed. If that company goes bankrupt, your money might disappear. If that company decides to censor you, you’re silenced. If that company changes its rules, you have no choice but to accept.

The Double Spend Problem

Before blockchain, digital money had a fundamental problem: digital files are easy to copy.

If I send you a digital dollar, how do you know I didn’t also send that same dollar to someone else? With physical cash, once I give it to you, it’s gone. With digital files, I can keep copies.

Banks solved this by keeping central ledgers – a master list of who has what. But that means trusting the bank.

Blockchain’s Solution

Blockchain solves all these problems by creating a shared, tamper-proof record that everyone can verify but no one controls.

No single person owns it. No single company runs it. No single government controls it. It just… exists, maintained by thousands of independent participants.

Key Insight: Blockchain isn’t just technology. It’s a new way of establishing trust. Instead of trusting people or institutions, we trust mathematics and code.

The Google Docs Analogy (The Best Explanation)

This is the analogy that made blockchain click for me. Let me share it with you.

Traditional Document (The Old Way)

I create a document on my computer. If I want you to see it, I email it to you. Now you have your own copy.

If I make changes, you don’t see them unless I email a new version. If we both edit at the same time, things get messy. One of us has the “master copy.” We have to coordinate, take turns, or constantly send updates.

Google Doc (The Shared Way)

We both open the same document online. We can both see it, both edit it, and both see each other’s changes instantly.

There’s only one document, but we both have access. No one “owns” it in the traditional sense. Google hosts it, but we both trust Google to show the right version.

The Blockchain Twist

Now imagine that instead of Google hosting the document, thousands of computers around the world each host a copy. Every time anyone makes a change, all copies update simultaneously.

To change something that was written yesterday, you’d need to change every single copy across thousands of computers, owned by thousands of different people, in different countries at exactly the same time.

That’s practically impossible.

Why This Analogy Works

| Traditional Document | Google Doc | Blockchain |

|---|---|---|

| One copy, one owner | One copy, shared access | Thousands of copies, no owner |

| Changes require permission | Changes visible to all | Changes require consensus |

| Can be lost or corrupted | Google keeps it safe | Network keeps it safe |

| Trust the owner | Trust Google | Trust mathematics |

The Key Difference

Unlike a Google Doc, blockchain has no central company like Google. It’s completely decentralized, run by everyone, owned by no one.

If Google goes down, your document might be temporarily unavailable. If half the nodes in a blockchain go down, the network keeps running. There’s no “off switch.”

How Blockchain Works (Step by Step)

Now let’s look at the actual process. Don’t worry we’ll keep it simple.

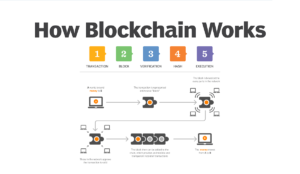

The Six Simple Steps

Step 1: Someone Requests a Transaction

It starts when someone wants to record something – send money, register an asset, or store data. This creates a “transaction” that gets broadcast to the network.

Step 2: Transaction Broadcast to Network

Think of shouting in a crowded room. The transaction is sent to thousands of computers (nodes) simultaneously.

Step 3: Nodes Verify the Transaction

Each computer checks:

- Does the sender have enough funds? (for cryptocurrency)

- Is the signature valid?

- Does it follow the network’s rules?

If yes, it passes initial verification.

Step 4: Verified Transactions Form a Block

Verified transactions are grouped together into a “block.” Think of a block like a page in a ledger book. Each block contains:

- A list of transactions

- A timestamp

- A unique fingerprint (hash) of the previous block

- A solution to a complex math puzzle (for Proof of Work systems)

Step 5: The Block is Added to the Chain

Nodes agree the block is valid through consensus (more on this shortly). Once agreed, the block is added to all previous blocks, forming a “chain.”

Each new block strengthens the security of all previous blocks. It’s like adding another link to a chain. The chain gets stronger, not weaker.

Step 6: Transaction is Complete

The transaction is now recorded permanently. It can never be altered or removed. Anyone can verify it exists, anytime, anywhere.

Simple Summary

Transactions → Broadcast → Verification → Block → Chain → Permanent Record

Key Concepts Explained Simply

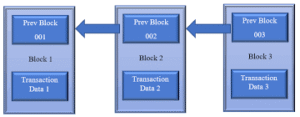

What is a Block?

A block is like a page in a ledger book. It contains:

- Data: The transactions or information being recorded

- Hash: A unique digital fingerprint (like a social security number for this specific block)

- Previous Hash: The fingerprint of the block before it (this is what creates the chain)

The Hash Analogy

Think of a hash like a wax seal on an old letter. If anyone opens the letter (changes the data), the seal breaks (the hash changes). Everyone can see it’s been tampered with.

A hash is created by a mathematical function that:

- Always produces the same output for the same input

- Produces a completely different output if even one character changes

- Cannot be reversed (you can’t figure out the input from the output)

What is the Chain?

The chain is what makes blockchain tamper-proof.

Each block contains the hash of the previous block. This links them together like you guessed it a chain.

The Domino Effect

If someone changes an old block, its hash changes. But that hash is stored in the next block. So that next block’s hash would need to change. Which would affect the block after that. And the next. And the next.

Changing one block means changing every block after it across thousands of computers, worldwide.

It’s like trying to change one page in every copy of every history book in every library on Earth.

What are Nodes?

Nodes are the computers that run the blockchain software. Each node keeps a complete copy of the entire blockchain.

There are thousands of nodes worldwide, all independently verifying every transaction.

Why Many Nodes Matter

- Redundancy: If some nodes go down, the network continues

- Security: To hack the blockchain, you’d need to control most nodes

- Democracy: No single node has special power. They’re all equal

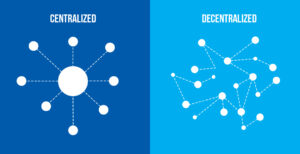

What is Decentralization?

Decentralization means no single person, company, or government controls the blockchain. Power is distributed across all nodes.

| Centralized | Decentralized | |

|---|---|---|

| Your bank account | Bitcoin blockchain | |

| Facebook’s servers | Ethereum network | |

| Company database | Public blockchain | |

| One decision-maker | Community consensus |

What is Consensus?

Consensus is how nodes agree on what’s true. Before adding a new block, nodes must agree it’s valid. Different blockchains use different consensus mechanisms.

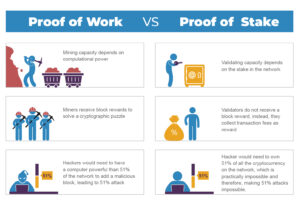

Proof of Work (Used by Bitcoin)

Miners compete to solve complex math puzzles. The first to solve gets to add the next block and earn rewards.

- Pros: Extremely secure, battle-tested for 15+ years

- Cons: Uses lots of electricity

Proof of Stake (Used by Ethereum now)

Validators lock up (stake) their own coins as collateral. They’re chosen to add blocks based on how much they’ve staked. If they cheat, they lose their stake.

- Pros: Uses 99.9% less energy, faster

- Cons: Newer, different security assumptions

Types of Blockchains

Not all blockchains are the same. Here are the main types:

| Type | Who Can Read? | Who Can Write? | Who Can Verify? | Examples |

|---|---|---|---|---|

| Public (Permissionless) | Anyone | Anyone | Anyone | Bitcoin, Ethereum |

| Private (Permissioned) | Restricted | Restricted | Restricted | Company internal |

| Consortium | Varies | Selected group | Selected group | Banking networks |

| Hybrid | Varies | Varies | Varies | Mix of both |

Public Blockchains (Open to Everyone)

Anyone can join, read, write, and verify. No permission needed. Completely decentralized. This is what most people mean by “blockchain.”

Pros

- Censorship-resistant

- Transparent

- No single point of failure

Cons

- Slower (must achieve global consensus)

- Less privacy

- Can be expensive during congestion

Private Blockchains (Company-Controlled)

A single organization controls the network. Participants need permission. Not truly decentralized, more like a shared database with blockchain features.

Pros

- Faster (fewer nodes to agree)

- More privacy

- Lower costs

Cons

- Must trust the controller

- Single point of failure

- Not censorship-resistant

Consortium Blockchains (Group-Controlled)

A group of organizations shares control. Common in banking and supply chains where multiple companies need to trust shared data but don’t want public access.

Examples

- R3 Corda (banking)

- Hyperledger (enterprise)

- Energy Web Foundation (energy sector)

Which One Matters for Crypto?

When people talk about cryptocurrency, they mean public blockchains. Bitcoin and Ethereum are public. Anyone can use them, no permission needed.

Blockchain vs Traditional Databases

| Feature | Traditional Database | Blockchain |

|---|---|---|

| Control | Centralized (one administrator) | Decentralized (no single controller) |

| Data modification | Can edit, delete, overwrite | Append-only (can only add) |

| Transparency | Hidden from public | Publicly verifiable |

| Trust model | Trust the administrator | Trust the code and consensus |

| Speed | Very fast | Slower (minutes for Bitcoin) |

| Censorship resistance | Administrator can censor | Nearly impossible to censor |

| Single point of failure | Yes (server down = system down) | No (thousands of nodes) |

| Cost | Operational costs | Transaction fees |

The Key Differences Explained

1. Who’s in Charge?

With a database, someone has the master password. They can change anything. With blockchain, no one has master control, changes require network agreement.

2. Can Data Be Changed?

Databases let you edit or delete. Blockchains only let you add new data. Old data stays forever. This is why blockchain is called immutable.

3. Who Can See the Data?

Databases are usually private. Public blockchains are completely transparent. Anyone can view any transaction ever made.

When to Use Each

Use a traditional database when:

- You need speed (millions of transactions per second)

- You trust the administrator

- You might need to edit or delete data

- Privacy is required

Use a blockchain when:

- Multiple parties need to trust shared data

- You need permanent, tamper-proof records

- No single party should control the data

- Transparency is valuable

Key Takeaway: Blockchain isn’t better than databases for everything. It’s better for specific situations where trust, transparency, and decentralization matter more than speed.

Why Blockchain is Secure

The Three Pillars of Blockchain Security

1. Cryptographic Hashing (Tamper Evidence)

Every block has a unique fingerprint (hash) created by a mathematical function. Change even one character in the block, and the hash changes completely.

It’s like a tamper-evident seal. Anyone can see if data has been altered.

How Hashing Works

- Input “Bitcoin” → Output “6b88c…”

- Input “bitcoin” (lowercase b) → Completely different hash

- Impossible to reverse (can’t get original from hash)

- Same input always produces same output

2. The Chain Structure (Tamper Resistance)

Each block contains the hash of the previous block. This links them together like a chain. To change a historical block, you’d need to recalculate all subsequent blocks – a computational nightmare.

3. Decentralization and Consensus (Tamper Prevention)

Even if a hacker could recalculate all blocks (extremely difficult), they’d need to convince the network their version is correct. With thousands of independent nodes worldwide, this is practically impossible.

The 51% Attack (Theoretical Risk)

If someone controlled more than 50% of the network’s computing power (Proof of Work) or staked coins (Proof of Stake), they could potentially manipulate the blockchain.

For major blockchains like Bitcoin and Ethereum, this would require billions of dollars and is considered extremely unlikely. The cost of attacking the network exceeds any possible gain.

What This Means for Users

- Your transactions can’t be reversed without your consent

- No one can delete or alter history

- The network has never been hacked (Bitcoin: 15+ years, Ethereum: since 2015)

- Your security depends on protecting your private keys, not trusting the network

Real-World Analogy: Think of blockchain security like a massive fortress with thousands of guards. To break in, you’d need to bribe most of the guards simultaneously. But unlike a fortress, these guards don’t communicate, they’re independent, making coordinated bribes nearly impossible.

Real-World Blockchain Use Cases

Beyond Cryptocurrency

While blockchain is famous for Bitcoin, its potential applications are much broader.

Cryptocurrency and Payments (The Original Use)

Bitcoin, Ethereum, and thousands of other cryptocurrencies use blockchain to enable peer-to-peer digital cash. No banks required.

Smart Contracts and DeFi

Ethereum added programmability, enabling automatic agreements (smart contracts) and decentralized finance. Lending, borrowing, and trading without banks.

Supply Chain Tracking

Companies use blockchain to track products from origin to store:

- Walmart: Tracks food sources to quickly identify contamination (reduced tracing time from 7 days to 2.2 seconds)

- De Beers: Tracks diamonds from mine to buyer (conflict-free certification)

- FedEx: Tracks high-value shipments

- IBM Food Trust: Used by multiple food companies

Healthcare Records

Patients could control their medical records, granting access to doctors as needed. Estonia already uses blockchain for healthcare data, securing over a million patient records.

Digital Identity

Self-sovereign identity lets you control your personal data instead of companies. You can prove you’re over 21 without sharing your exact birthdate.

Voting Systems

Blockchain could enable secure, transparent, verifiable voting – reducing fraud and increasing trust. Several countries are experimenting.

- Sierra Leone (2018) tested blockchain voting

- West Virginia (2018) pilot for overseas military voters

- Switzerland (multiple cities) blockchain voting trials

Real Estate and Property Records

Land titles recorded on blockchain can’t be forged or lost. Countries like Georgia, Sweden, and Brazil are testing this.

Intellectual Property and Royalties

Artists can register work on blockchain and receive automatic royalties when it’s used or resold. Every time an NFT is resold, the original artist gets paid automatically.

Academic Credentials

Diplomas and certificates on blockchain are instantly verifiable, eliminating fake degrees. MIT has issued digital diplomas to graduates since 2017.

Charity and Aid

Donors can track exactly how their money is used, ensuring it reaches intended recipients. UN World Food Programme uses blockchain to deliver aid to refugees.

Blockchain Beyond Crypto

The Enterprise Adoption Wave

Major companies and governments are now building blockchain solutions, even if they don’t talk about cryptocurrency.

| Company/Organization | Use Case |

|---|---|

| IBM | Food Trust (supply chain with Walmart) |

| Microsoft | Azure Blockchain (enterprise platform) |

| Amazon | Managed Blockchain (AWS service) |

| JPMorgan | Onyx (blockchain for banking) |

| Walmart | Food safety tracking |

| Maersk | Shipping documentation |

| Dubai government | All government documents |

| European Union | Blockchain for cross-border services |

The Difference in Approach

- Crypto blockchain: Public, permissionless, decentralized, open to everyone

- Enterprise blockchain: Often private or consortium, permissioned, controlled by known entities, faster but less decentralized

Why Enterprises Care

- Efficiency: Shared data reduces reconciliation costs

- Transparency: All parties see the same information

- Trust: No single company controls the data

- Automation: Smart contracts reduce paperwork

The Future

Blockchain is becoming infrastructure, like the internet. You might not see it, but it will power many systems you use. Just as you don’t think about TCP/IP when you send an email, you won’t think about blockchain when you verify a document, track a package, or prove your identity.

Common Blockchain Myths

Myth 1: “Blockchain and Bitcoin are the same thing”

Reality: Bitcoin is the first application of blockchain technology. Blockchain is the underlying technology. Like how email is an application of the internet.

Myth 2: “Blockchain is completely anonymous”

Reality: Most blockchains are pseudonymous. Transactions are public and linked to addresses, not names. But with analysis, transactions can often be traced, especially through exchanges that require ID.

Myth 3: “Blockchain can’t be hacked”

Reality: The blockchain itself is extremely secure, but surrounding systems (exchanges, wallets, smart contracts) can be hacked. The Bitcoin network has never been hacked; individual wallets have been.

Myth 4: “All blockchains are public”

Reality: Private and consortium blockchains exist, where access is restricted to approved participants. These are popular with businesses.

Myth 5: “Blockchain is too slow for real-world use”

Reality: Base layer can be slow (Bitcoin: 7 transactions/second), but Layer 2 solutions and newer blockchains achieve thousands per second. Visa processes about 1,700/second. Many blockchains now exceed this.

Myth 6: “Blockchain wastes energy”

Reality: Proof of Work (Bitcoin) uses significant energy. But Proof of Stake (Ethereum now) uses 99.9% less energy. Not all blockchains are energy-intensive.

Myth 7: “Blockchain will replace all databases”

Reality: Blockchain is better for specific use cases requiring trust among multiple parties. For most internal company needs, traditional databases are faster and cheaper.

Myth 8: “Once data is on blockchain, it’s there forever”

Reality: Data on public blockchains is permanent. This is a feature for some use cases, a drawback for others (like storing illegal content or private data).

Myth 9: “Blockchain is too complex for normal people to use”

Reality: You don’t need to understand blockchain to use it. Just like you don’t need to understand SMTP to send email. Wallets and apps abstract away the complexity.

Myth 10: “Blockchain is a bubble that will pop”

Reality: Blockchain technology continues to be adopted by major companies and governments. Individual cryptocurrencies may be volatile, but the underlying technology is here to stay.

Next Steps: From Blockchain to Bitcoin

You now understand blockchain – the technology that powers cryptocurrency. Here’s where to go next:

The Beginner’s Path

| Step | Action | Resource |

|---|---|---|

| 1. See Blockchain in Action | Explore a blockchain explorer like Etherscan or Blockchain.com | Etherscan |

| 2. Learn About Bitcoin | The first and most famous blockchain application | What is Bitcoin? |

| 3. Explore Ethereum | Programmable blockchain with smart contracts | What is Ethereum? |

| 4. Get a Wallet | Experience blockchain firsthand | Wallet Guide |

| 5. Make Your First Transaction | Buy a small amount of crypto | Best Crypto Exchanges 2026 |

Recommended Next Reads

- 📚 What is Bitcoin? A Beginner’s Guide

- 💜 What is Ethereum? Understanding Smart Contracts

- 📖 Complete Cryptocurrency Guide for Beginners

Final Thought

When I first learned about blockchain, the Google Docs analogy made it click. But what really drove it home was actually using it – sending a small amount of Bitcoin, watching the transaction appear on a block explorer, and realizing that this record would exist forever, maintained by thousands of computers I’d never see.

Blockchain is one of those rare inventions, like the internet itself that will take decades to fully understand and apply. You’ve taken the first step. The journey continues.

Disclosure: This guide is for educational purposes only. Blockchain technology is complex and evolving – this explanation simplifies concepts for beginners while maintaining accuracy.

This guide was last updated for the 2026 edition. Blockchain technology evolves rapidly – check back for updates, and always verify information with multiple sources before making decisions based on this technology.

Frequently Asked Questions

How does blockchain work?

Transactions are grouped into "blocks." Each block is cryptographically linked to the previous one, forming a "chain." Thousands of computers (nodes) each keep a copy and must agree before new blocks are added.

Is blockchain safe?

The blockchain technology itself is extremely secure. Major blockchains like Bitcoin have never been hacked. However, apps built on blockchain (exchanges, wallets, smart contracts) can have vulnerabilities.

What's the difference between blockchain and Bitcoin?

Bitcoin is a digital currency. Blockchain is the technology that makes Bitcoin work. Think of blockchain as the railroad and Bitcoin as a train running on it.

Can blockchain be hacked?

Theoretically, if someone controlled more than half the network's computing power (51% attack), they could manipulate recent transactions. For major blockchains, this is prohibitively expensive. The core blockchain has never been successfully hacked.

Who controls a blockchain?

No one controls a public blockchain. It's governed by consensus among all participants. Changes require agreement from the community. No single person or company has special power.

What are blocks in blockchain?

Blocks are like pages in a ledger book. Each block contains a batch of transactions, a timestamp, and a cryptographic link to the previous block.

What is decentralization in blockchain?

Decentralization means no single entity controls the system. Power is distributed across thousands of independent computers worldwide, making the system resilient to attack or censorship.

What are real-world uses of blockchain?

Beyond cryptocurrency, blockchain is used for supply chain tracking, healthcare records, digital identity, voting systems, real estate records, academic credentials, and more.

How is blockchain different from a regular database?

Databases have a central administrator who can edit or delete data. Blockchains are decentralized and append-only. You can only add data, never remove it.

What is a node in blockchain?

A node is a computer that runs blockchain software, keeping a complete copy of the ledger and verifying transactions. More nodes = more security.

What is mining in blockchain?

Mining is the process of adding new blocks in Proof of Work systems (like Bitcoin). Miners compete to solve complex math problems; the winner adds the block and earns rewards.

What is Proof of Stake?

Proof of Stake is an alternative consensus mechanism where validators lock up (stake) their own coins as collateral. They're chosen to add blocks based on their stake, using far less energy than mining.

Is blockchain private?

Public blockchains are completely transparent. Anyone can view all transactions. Private blockchains restrict access to approved participants.

What's the future of blockchain?

Blockchain is expected to become foundational infrastructure, like the internet. It will likely power many systems behind the scenes without users even knowing.